One of the unexpected benefits of working overseas early in my career was learning about investors I probably wouldn't have come across until much later on. British investors like Nick Train, Neil Woodford, and Terry Smith, for example, have influenced my investment philosophy in some fashion.

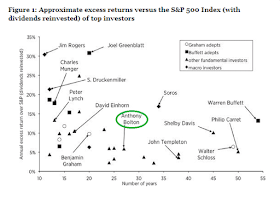

The subject of today's post, Anthony Bolton, also fits into this group. Bolton ran the Fidelity Special Situations Fund in the U.K. for 28 years ending December 2007, posting incredible annualized returns near 19.5% while at the helm.

Suffice it to say, there's a lot we can learn from Bolton.

His tenure coincided with another famous Fidelity fund manager, Peter Lynch, whose foreword to Bolton's book, Investing Against the Tide: Lessons From a Life Running Money was alone worth the price of admission.

was alone worth the price of admission.

Here are a few lines from Lynch's foreword:

The subject of today's post, Anthony Bolton, also fits into this group. Bolton ran the Fidelity Special Situations Fund in the U.K. for 28 years ending December 2007, posting incredible annualized returns near 19.5% while at the helm.

His tenure coincided with another famous Fidelity fund manager, Peter Lynch, whose foreword to Bolton's book, Investing Against the Tide: Lessons From a Life Running Money

Here are a few lines from Lynch's foreword:

- To succeed in investment you have to work at it. Watch for the importance of hard work as you turn these pages. Note how often going the extra mile on research and analysis is what accounts for sustained success. Keep your eye on that theme and you'll see that what the media call investment "genius" actually springs from a base of sustained, unending research - which, in turn, yields a decisive information edge. That edge, plus steady nerves, flexibility, good judgement and a complete lack of bias or prejudgement is what has enabled Anthony Bolton to deliver record-setting compound returns for decades. (my emphasis)

- I stress hard work, an information edge and flexibility because few cliches have done more damage to investors' wealth than the phrase 'play the market'.

- What distinguishes investment winners...is the willingness to dig deeper, search more widely and keep an open mind to all ideas - including the idea that you might have made a bad call. He or she who turns over the most rocks, looks over the most investment ideas, and is unsentimental about pas choices is most likely to succeed.

The book's worth a read for intermediate and advanced investors. The organization is messy, unfortunately, but there's rich content inside. Bolton's recollection of company meetings serve up some great lessons. Those managing money will appreciate his thoughts on portfolio management, as well.

Here are 13 gems I double-highlighted while reading the book.

- Often, I ask myself a very simple question: 'How likely is this business to be around in ten years' time and to be more valuable than today?' It's surprising how many businesses fail this test.

- Sometimes the names of the institutional shareholders (of a company) will carry information because there are some I rate more highly than others and if one or two I rate are on the list that's a positive.

- The ultimate commendation is when a company talks positively about a competitor...In fact, as a general rule, when a company says the opposite of what you expect them to say I put a double weight on it.

- (Good managers) tend to be fanatical about the business, working long hours and demanding high performance and excellence from their team and they are reasonably self-assured and on top of what they do without being arrogant.

- Seeing through spin is one of the most important aspects of the job.

- I prefer thinking in levels of conviction rather than in price targets.

- The (stock) price itself influences behaviour - falling prices create uncertainty and concern, rising prices create confidence and conviction. Understanding this is a really important part of investing.

- A portfolio should, as nearly as possible, reflect a 'start from scratch' portfolio...One of the things I do each month is an exercise that helps me measure my conviction. On a piece of paper I write five headings across the top: "strong buy", "buy", "hold", "reduce" and "?"

- I don't normally make large adjustments to the size of my holdings in one go, my moves are incremental.

- When I've analysed the biggest mistakes I've made over the years they have nearly always been in companies with poor balance sheets.

- Thinking like a short specialist is a good discipline for most portfolio managers...If you are aware of what might go wrong in a company (knowing the counter investment thesis) one may be able to spot before others the fact that it is going wrong.

- It's rare that you only get one chance to make a trade at a specific level.

- I've always thought that the best environment in which a fund manager could perform well was one in which they didn't know how they were doing.

Earlier this year, I was invited by Harriman House publishers to contribute a chapter to their forthcoming book, Harriman's New Book of Investing Rules: The do's and don'ts of the world's best investors

Earlier this year, I was invited by Harriman House publishers to contribute a chapter to their forthcoming book, Harriman's New Book of Investing Rules: The do's and don'ts of the world's best investors