"Charles Ellis: Turning now to individual investors, do you think that they are at a disadvantage compared with the institutions, because of the latter's huge resources, superior facilities for obtaining information, etc.? Benjamin Graham: On the contrary, the typical investor has a great advantage over the large institutions." - 1976 Interview with Benjamin Graham

Every so often, particularly after I've made an error in judgement, I consider selling my individual stocks and going 100% into index funds. Just think of all the time I'd save not researching on the weekend...

Eventually I come to my senses and remember that any extra time saved would probably be spent on a golf course, growing increasingly frustrated by a series of 200 yard slices into the woods and three-putts. But I digress.

Invest long enough and doubt inevitably creeps in. Frankly, I'd be concerned if you didn't doubt yourself now and then. Overconfidence is not a long-term asset in the investing world.

You're going to make some mistakes along the way, but the key is to make mistakes while exploiting your advantages as an individual investor. As Charles Ellis noted in his question to Ben Graham, institutions have a number of advantages over individuals, so there's little point to going toe-to-toe with them on their home turf. Instead, focus on areas where you, the individual investor, have natural advantages.

Patience and independence

The first advantage is really what this blog is dedicated to: the individual investor's ability to be patient and think long-term.

Institutional investing is very much a "What have you done for me lately?" business and fund managers are frequently compared with the performance of their peers and their benchmark. Your fund could generate 50% returns in a year, but if your peer group generated 60% returns, brace yourself for cash outflows.

In fact, a recent study on Warren Buffett's track record found that his ability to survive extended periods of market underperformance -- due to his reputation and unique operating structure as a corporation -- played a key role in his results. Most institutional investors don't enjoy similar advantages and are thus required to focus on short-term results while not deviating too far (on the downside) from the peer group.

Individual investors, on the other hand, don't have to worry about underperforming in a given year and can thus maintain a patient and long-term focus. You can hold a large cash position or take a contrarian position, for instance, and give your thesis a few years to play out without worrying about investors pulling money out of your fund.

Making meaningful investments in smaller companies

In the 1995 Berkshire Hathaway letter, Buffett wrote: "The giant disadvantage we face is size: In the early years, we only needed good ideas, but now we need good big ideas." In order to have a meaningful impact on results, institutional investors with hundreds of millions under management need to make large investments. As assets under management increase, fund managers find it difficult to make large investments in small companies without dramatically increasing the share price or taking an unwanted controlling stake in the company.

As a result, institutional investors are forced buy a lot of small stakes in small companies or focus on large companies. In either case, their opportunity to consistently generate high compounding growth rates is more limited than it is for individual investors who can take meaningful positions in promising smaller companies.

Given the advantage of having less capital, individual investors -- even those favoring dividend-paying stocks -- shouldn't be afraid to look for small cap opportunities that fit your normal investing criteria.

The ability to think like business owners

The short-term performance pressures on institutional investors also limits their interest in taking the perspective of a business owner in the stocks they are buying. If you're going to sell the stock in a few weeks or months, why bother worrying about management's incentives? (Indeed, Vanguard founder Jack Bogle has called this out as one of the reasons for a declining sense of corporate governance and responsibility, but that's a separate topic.)

Conversely, with no such performance pressures, individuals can invest in companies in which they'd like to take a long-term, business-focused position. This requires a differentiated research process -- one that focuses on things like the company's durable competitive advantages, management's capital allocation skill, and the board's dividend policy.

Bottom line

Though it may not always be apparent, individual investors have a number of advantages over institutional investors. Mistakes and frustrations are a part of investing, but if you're going to err, err while pursuing these advantages -- namely, the ability to be patient and independent, invest in a wider universe of stocks, and take the perspective of a business owner.

This will be the last Clear Eyes Investing post in 2013 and I just wanted to say "thank you" for reading this year. The blog eclipsed 50,000 page views earlier this month, which is about 50,000 more than I ever expected when I started writing last year. I particularly appreciate the frequent references from your own blogs and those of you who've shared my posts via email and social media. Merry Christmas and a Happy New Year! Todd

Warren Buffett's meeting with University of Maryland MBA students - Dr. David Kass

What history tells us about investing in dividend income stocks - Investment Moats

Why closet index trackers need to be relegated out of existence - UK Value Investor via Stockopedia

Quote of the week:

There is a set of advantages that have to do with material resources, and then there is a set that have to do with the absence of material resources -- and the reason underdogs win as often as they do is that the latter is sometimes every bit the equal of the former. - Malcolm Gladwell, David and Goliath

"Ultimately, nothing should be more important to investors than the ability to sleep soundly at night." - Seth Klarman

In a recent post about becoming a more patient investor, one of the tips I shared was to stay reasonably diversified because having a highly-concentrated portfolio would likely keep you up at night and lead to impatient trading decisions.

Upon further reflection, this advice was a bit off the mark as it was specific to my own investing personality and isn't a universal law. For other investors, a highly-concentrated portfolio of thoroughly-researched investments may provide them more than enough comfort, while others may only feel comfortable in broadly-diversified index funds.

Homer gets it

Each investor's risk-taking personality is different -- it could be in our genes -- but the key is to invest in a manner that lets you sleep at night without worrying what the next trading day, week, or month might bring.

At the core of this discussion is anxiety produced by our investment decisions. Losing sleep may be a consequence of the anxiety -- it can also manifest itself in nail biting, smoking, pacing, or at worst, panic attacks -- but it's the root cause of what we need to avoid as patient investors.

When we're anxious as investors, we're not acting as investors at all -- we're simply speculating and we're much more prone to making destructive short-term decisions.

Thinking about it this week, I see five main causes for undue investment-related anxiety:

Investing outside of your core competency: Remember Peter Lynch's principle #5: "Never invest in any idea that you can't illustrate with a crayon." If you don't understand the business, you're more likely to become overly concerned about temporary issues or not concerned enough about long-term issues.

Not doing your own research: Whether you're getting investment ideas from a friend, newsletter, or financial website, it's important to look into the company yourself and decide whether or not you agree with the idea. There are pretty good odds you're not going to miss the opportunity if you wait 24 hours after hearing the idea to do your own research.

Employing unsuitable amounts of leverage: For the individual investor, leverage most often comes in the form of margin borrowing or options strategies. While both of these tools in themselves are not bad, they can serve to magnify both gains and losses and should be used with caution.

Being a forced buyer or seller: One advantage of being an individual investor is that we typically don't need to be forced buyers or sellers as we don't have clients giving and taking money to and from our funds on a regular basis. Still, we can fall victim to being a forced trader when inappropriately using leverage or investing short-term money in long-term assets.

Reaching for return: In The Most Important Thing, Howard Marks recalls, "It's remarkable how many leading competitors from our early years are no longer leading competitors (or competitors at all). While a number faltered because of flaws in their organization or business model, others disappeared because they insisted on pursuing high returns in low-return environments." This a particularly important point to remember in today's market and dividend investors, for example, who are reaching for ultra high yields (more than 2.5x the market average) are exposing themselves to ultra high risks.

Why aren't market movements one of the causes of anxiety? Don't get me wrong, I don't enjoy seeing my portfolio lose money any more than the next person, but if we truly are patient long-term investors and can avoid subjecting ourselves to the five root causes of investment-related anxiety, short-term fluctuations shouldn't result in unmanageable levels of anxiety. In fact, we can even use Mr. Market's anxiety to our advantage by being prepared to buy when he's despondent and sell when he's euphoric.

There are countless investment quotes and sayings worth keeping in mind, but the Klarman quote at the beginning of this post is one of the dozen or so that's worth worth writing down and keeping near your desk. It's a good reminder to always invest in a manner that lets you avoid high levels anxiety as it will allow you to stick to your strategy regardless of what the market is doing in the short-term.

I've created a Facebook page for the Clear Eyes Investing blog. If you enjoy the content here and would like to be updated via Facebook when new posts are published, please "like" it! Good reads this week:

Even though the tag-line of the Clear Eyes Investing blog is, "Patience is the individual investor's greatest advantage over the market," patience is a virtue that doesn’t come naturally to me.

Maybe I played too much Nintendo as a kid or something, but my default expectation is for instant results. Whenever I’m stuck in highway traffic or waiting for a commuter train that’s running behind schedule on a frigid Chicago morning, I have to remind myself to stay calm and not get stressed, for it’s in such times that I’m prone to make stupid decisions. Thankfully, I’m not alone in this. As Michael Mauboussin has noted in variousarticles, when we’re stressed, our mental time horizon shrinks and we have a tendency to make decisions that are completely focused on short-term results and we disregard long-term effects. Our brain’s reaction to stress may serve us well at times of imminent physical danger, but it can be really destructive when it comes to our financial health. By reducing our investing stress and increasing our investing patience, I believe we can truly improve our long-term results. Indeed, hedge fund manager Joel Greenblatt recently said as much in a Morningstar interview:

"The secret to value investing is patience, and that's generally in short supply now...The world is becoming more institutionalized, there is more access to performance information, it's much easier to trade. So, patience is in short supply, and it really makes it much nicer for patient value investors…(Value investing) works over time, and it's quite irregular. But it does still work like clockwork; your clock has to be really slow." (My emphasis)

What are some ways that we can improve our ability to be patient? I’ve started a list here, but would also enjoy hearing your tips in the comments section below (or let me know on Twitter).

Make a list of things that stress you out when investing: Knowing exactly what your stress triggers are will help you recognize them as they occur. One of my triggers, for example, is when a company I own makes a large acquisition that has a good chance of being value destructive. My instinct is to sell first and ask questions later, but the opposite has proven to be the better approach.

Buy right and sit tight: Loss aversion is a powerful force -- and humans tend to feel the pain of a loss twice as much as the joy from a gain. In fact, some people are more sensitive to losses than others. As such, much of the investing stress that I’ve experienced myself and have heard from others comes on the selling end of an investment. Not knowing the right time to sell -- even if it will produce a gain -- can indeed be stressful. Howard Marks shared in his book, The Most Important Thing that Oaktree Capital employs the philosophy that "Well bought is half sold.” In other words, if you pay good prices for your investments, the selling should take care of itself (and be a lot less stressful).

Have a 24-hour trading rule: If you’re feeling strong emotions before placing a trade -- excitement, agony, stress, etc. -- having a 24-hour trading rule can help you make calmer, more rational decisions. Take the time to consider why exactly you want to buy or sell this particular stock. You may still end up placing the trade the next day, but it will be done with more thought and less emotion.

Establish longer-term performance benchmarks: Short-term investment performance has much more to do with luck than skill; therefore, it seems much more appropriate to judge our investments over a 3-5 year period rather than by a month or quarter. Granted, an investment thesis could completely fall apart within a year and action may be warranted, but aiming to give each investment a few years to play out before we sell it should reduce the need to impatiently sell based on short-term performance.

Take stock quotes off your smartphoneor internet homepage: There was a time not too long ago where you had to either call your (expensive) broker or wait for the daily newspaper to get the latest quote on your stock. With real-time quotes at our fingertips these days, I'd bet that those flashing green and red lights cause us to make more frequent trading decisions that we would otherwise. If you’re finding this to be the case in your own portfolio, try going without real-time quotes for a while and see if that helps.

Stay diversified (to a point): Some investors will say that in order to really trounce the market, you need to have a very concentrated portfolio of just a few holdings that you really believe in. Perhaps there’s some truth to that, but there’s also something to be said for being able to sleep at night. As confident as I might be in a thesis, I also know that I’m fallible, so as a rule I don’t invest more than 10% of my portfolio in a single name. Having such a big bet on a single company would likely cause me to be impatient if my thesis wasn’t working out and make hasty trades.

Read and re-read the classics: Regardless of how the market is behaving at a given time, remember that it’s happened before. The circumstances may be different, but investor behavior is the same. When in doubt about the current state of the markets, consult The Intelligent Investor, the annual Berkshire Hathaway letters, and just about any book on this list really. During the financial crisis, for example, Jack Bogle’s reflections on Wellington Fund’s 75th birthday helped me maintain my long-term approach during a very difficult time in the market.

Find a “support” group: Most of the financial content on the internet is designed for short-term traders, but there are plenty of patient, long-term investors out there on various blogs (see a list of good blogs on the right), message boards, and websites that would be happy to help you work through an investment decision if you’re having trouble or have a question. Including this one!

Start an investment journal: One of the best tips I received was to start an investment journal in which I wrote down my investment thesis, risks, and any emotions or concerns I felt when placing the order. This will serve to reduce “thesis drift” and help you make more rational decisions when you’re not sure what to do about a certain investment.

A thing long expected takes the form of the unexpected when at last it comes. - Mark Twain

In such a low-interest rate environment, why would the market allow companies to trade with 8%+ free cash flow yields -- even after considering a reasonable equity risk premium?

The answer lies in market expectations. For firms with very low free cash flow yields, the market is expecting robust free cash flow growth in the coming years; conversely, for firms with high free cash flow yields, the market might be expecting some free cash flow contraction.

In this graphic, you could justifiably substitute "expectations" for "price".

Naturally, higher market expectations also carry greater risk for market disappointment, and vice versa. As we're evaluating companies for potential investment, this is an important relationship to bear in mind.

To illustrate, I considered the free cash flow yields of some of the largest S&P 500 stocks:

As the list illustrates, the market has relatively lower expectations for Apple than it does Home Depot and lower expectations for Wal-Mart than it does Tesla. This doesn't necessarily mean that Apple is a better investment than Tesla at the moment, but it does mean that, in terms of market expectations, Tesla has much less room to make a mistake than Apple does.

While some stocks with high market expectations -- the Teslas, Amazons, etc. -- could end up being great investments by doing even better than the market currently expects, I think that investors will do have better results, on average, by investing in companies with low market expectations.

Yes, those companies could also do worse than the market expects and fall further in price, but if we conclude that a company's competitive advantages remain intact, the financials are sound, and that they're led by capable management, then there are fairly decent odds that the market's low expectations are wrong.

Whether we're looking for long or short candidates, as investors we want to find where the market's expectations are meaningfully different from our own. Before you begin researching a new company or re-evaluating a current holding, then, it's helpful to determine the company's free cash flow yield to see where it sits on the market expectations spectrum and how your own expectations might differ.

Please note: I recently updated the blog's URL to www.cleareyesinvesting.com from cleareyesinvesting.blogspot.com. Existing bookmarks should work fine, but please let me know if you have any trouble accessing the site.

Good reads this week:

Ten Things I've Learned from Ten Years of Active Investing - Monevator

Investors May Clean Up With This Dividend Payer - Morningstar

Quote of the week:

This paradox exists because most investors think quality, as opposed to price, is the determinant of whether something’s risky. But high quality assets can be risky, and low quality assets can be safe. It’s just a matter of the price paid for them. - Howard Marks, "Everyone Knows"

“No, no! The adventures first, explanations take such a dreadful time.” - Lewis Carrol, Alice in Wonderland

At an investor conference a few weeks back, I had the pleasure of hearing a dozen or so companies tell their stories to rooms filled with potential investors. No matter how long you've been investing, there are always companies you haven't learned about yet and others with new stories to tell. That's one of the great things about this business -- it provides lifetime learning opportunities.

As I was sitting in the various rooms listening to the presentations, I couldn't help but think how powerful stories are in the investing world. After all, no one is eager to brag to their friends about the investment they just made in a company that treats sewage. It's far more fun to tell friends about a company whose new gadget will replace the need for burning fossil fuels, or some such thing.

Indeed, storytelling has always been a fundamental part of the human experience. Yet as investors, it's important that we learn to separate story from substance before we invest our hard-earned money in a company.

The first investment pitch? Note the bulls...

What I mean by this is that before we invest in a company we've read about in a magazine, newspaper, newsletter, etc., we need good answers to the following questions:

Why am I excited about this particular company? With any investment idea, there's always something that gets us interested. Perhaps it's the fact that the company is tapping into a major trend like 3D printing or that it's got a product that's sure to make the world a better place. Perhaps it's led by a CEO with a silver tongue. The key is to identify what exactly it is that got you interested, separate it from the larger narrative, and begin to draw your own conclusions about it. For example, you might say to yourself, "This company's product has huge potential, but five of their peers have come up with a similar product," or, "Looking at the CEO's track record, I've found that he gave a similarly optimistic pitch five years ago and the stock has underperformed the market."

Who doesn't already know this story? There are really good odds that you're not the first investor to hear about the company's story and, even if the story has substance, you most certainly don't want to be one of the last investors to hear about it. Have a look around the internet to see if there are other investors discussing the same story. If that's the case, you're too late.

What happens when the story changes? Blame it on the fact that I'm a history major, but when I'm researching a promising company, I always go back at least ten years and read the chairman and CEO letters in the annual reports to better understand why the company is where it is today. By doing this exercise, one thing you'll quickly pick up is that the narrative changes over time. Companies acquire and divest businesses, growth markets become mature markets, and so on. Try to determine management's record of delivering on expectations -- do they frequently over-promise to boost short-term investor interest only to under-deliver and disappoint in the long-term? If so, that's not a company worthy of your investment.

Do the numbers check out? Companies with durable competitive advantages should have numbers that reflect their position. How do the companies' margins, returns on capital, and free cash flow figures stack up against their peers? Also, keep a look out for potential pot-holes like a highly-leveraged balance sheet or off-balance sheet liabilities -- things that normally aren't a part of a company's sales pitch.

What's management doing with its own money? Its amazing how few executives, who are more than willing to buy the company's stock with shareholder money, are unwilling to do the same with their own. If management really believes in its story and current valuation, they'll put some of their own money to work, too.

Here's the key thing to remember after you hear an exciting company story -- don't invest right after hearing the pitch. Wait at least 24 hours and let the emotion dissipate before proceeding with your research. By doing so, you'll save yourself a lot of trouble and make better decisions.

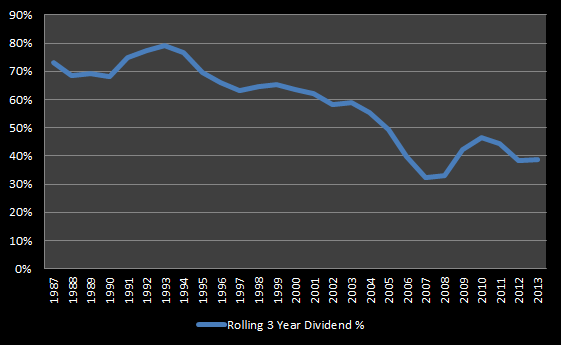

Prior to 1982, when large-scale share repurchases became viable after Congress enacted rule 10b-18, nearly all shareholder distributions were returned via cash dividends. As such, companies with longer operating histories tend to have a tradition of paying dividends and their shareholders have naturally come to expect them to continue. If given the chance, however, I suspect some of them would elect for a diminished dividend program in favor of buybacks, which offer substantially more financial flexibility and tend to benefit management and short-term investors. Consider the following chart, which shows the rolling three-year percentage of U.S. shareholder distributions made via cash dividends versus buybacks.

What's particularly notable is that this trend developed despite equal tax rates on dividends and long-term capital gains since 2003, an increasing number of retiring baby boomers seeking income over growth, and strong demand for higher-yielding stocks in a low rate environment. All of these factors should have encouraged a larger share of shareholder distributions going to cash dividends, but that's not happening. Some companies are clearly not comfortable with making a larger commitment to their dividend program. We can discuss the reasons this might be the case in the comments section below, but you might be rightly wondering at this point, "Why does this even matter?" As you're building a dividend portfolio, you want to stock it with companies that want to pay dividends. You don't want to own companies that feel burdened by their current payout, as these are the companies most likely to cut their payouts if given the opportunity. Here are five red flags that a company may not be comfortable with its dividend policy:

Token dividend increases: If a company's raising its dividend by a small amount each year (less than 4% growth), it might mean that it is cautious about its prospects, or it could mean that the company is simply raising its payout by a token amount to maintain a tradition of raising payouts. In either case, this is not an encouraging track.

High leverage and high payout ratio: Firms with high financial leverage that are also paying out the majority of free cash flow as dividends might be concerned about their ability to maintain the current payout. In the event of an economic downturn or a shock to their competitive environment, the dividend could come under fire. Keep an eye out for "token" dividend increases from such companies.

Excessive stock options in management compensation: The expected value of stock options decreases with the payment of dividends, so if the company's executive compensation program is heavily-weighted toward stock options, management may have a disincentive to paying higher levels of dividends.

Short-term focused ownership: If a friend or colleague offered you an opportunity to buy a small equity stake in a local business, one of the questions you'd surely ask is, "Who are the other owners?" You'd want to know how the other equity holders think about the business, are their interests aligned with yours, etc., yet it's amazing how infrequently this question is asked before investors purchase stocks. Take a look at the list of the company's largest shareholders (outlined in annual filings), check out the fund managers' websites, and try to determine if they're long-term and/or dividend-focused. If you see a bunch of hedge fund owners, you might want to walk away from the stock.

An increasing preference for buybacks: Though buybacks properly employed can support dividend growth, you want to see a balance between dividends and buybacks over time. If the company is shifting from a balanced approach toward more preference for buybacks, it's a warning sign that the company is losing enthusiasm for its dividend program.

As long-term, patient, dividend-focused investors, we want to own companies whose interests are aligned with our own. Recognizing the early signs of companies that are less committed to their dividend programs can help us better build our portfolios around the right companies.

Here's a general criticism that I often hear about investing in companies with economic moats:

Companies with economic moats always look expensive and they trade with premium multiples to the market. How can we invest with a suitable margin-of-safety and generate superior returns if we're consistently buying expensive stocks?

It's a fair criticism. Indeed, companies that can consistently out-earn their costs of capital should trade with premium multiples and frequently do. In bull markets such as this one, quality doesn't come cheap and good moat-buying opportunities seem far and few between.

But here's the key thing to remember -- economic moats affect value in the long-term while the market's focus is on short-term results.

Why does this matter? Because if we're patient investors -- and if you're reading this blog, you're probably in this camp -- we only need to wait for the market to overreact to some short-term news (a bad quarter, etc.) that doesn't impact the company's competitive position and then look to capitalize on the opportunity. In other words, use the market's short-termism to our long-term advantage.

Opportunities to buy quality companies at good prices do present themselves over the course of the business cycle -- and purchasing premium companies at market average prices is a strategy I'll gladly endorse.

Like most people, I don't like being wrong. Trouble is, I'm wrong quite often. To err is human, after all, and I've come to accept the fact that I'll make incorrect choices in the course of everyday life, such as the time I was about the head outside wearing both a corduroy jacket and corduroy trousers before my wife mercifully stopped me and corrected my obvious fashion misjudgment. When it comes to investing matters, however, I have yet to similarly come to terms with making incorrect choices. I tend to dwell on the mistakes I've made in my portfolio far more than I enjoy the successful moves I've made. A dent to my pride can be repaired, but a permanent loss of capital cannot. The key to managing investment mistakes, as I've come to learn the hard way, is to admit them quickly, correct the mistake, and use the expensive lesson to improve your investment process.

Admit them quickly: This is the hardest part. Your research and thesis turned out to be wrong, but it's easier to be stubborn and rationalize the mistake. In my own experience, I've found that writing down my thesis before purchasing a stock has helped me own up to my mistake and not succumb to "thesis drift."

Correct the mistake: Investors who've made a mistake often compound the mistake by either waiting for the market to correct it for them -- the classic, "I'll just hold on until the price gets back to my purchase price" -- or doubling-down on a broken thesis hoping the lower cost basis will fix things with time. In this situation, it's best to close your position and reallocate your capital to a better idea. (I should note here that if your thesis remains intact but the stock price has simply fallen a bit due to short-term concerns, that's not necessarily a mistake on your part and it may in fact be wise to hold or double down).

Improve your investment process: Do a post-mortem on your mistake. Determine where you went wrong with your research and/or thesis and apply the lessons to your process going forward. In fact, I recommend including a pre-mortem in your investment process and think about what could go wrong before you buy the stock. For instance, ask yourself, "If the stock falls by 50%, what happened?"

Investing is, by nature, a humbling endeavor and we can't always be right. In this business you're a legend if you're consistently right 6 out of 10 times, which still leaves 4 mistakes out of 10 to address. Acting as if the mistakes never happened doesn't do anyone any good. Instead, by learning to make the most of our investing mistakes -- while ultimately seeking to minimize their frequency -- I believe we can greatly improve our long-term results. Good reads this week Going for Long-Term Growth - Interactive Investor The First Law of Thermodynamics and Investing Risk - Monevator The Intersection of High Quality and Cheap Valuation - Fidelity Quote of the week "Life is not always a matter of holding good cards, but sometimes playing a poor hand well." – Jack London Thanks for reading! Best, Todd @toddwenning

Dividend investing can seem deceptively easy. If you want to generate, say, a 5% yield from your dividend portfolio, you only need to buy a group of stocks that provide a weighted average yield of 5%. Then just sit back and watch the money roll in.

Or so the thinking goes.

And, yes, you may indeed receive your desired dividend income if you follow this strategy, but constructing a portfolio in this manner without attention to valuation could end up costing you in the longer-term.

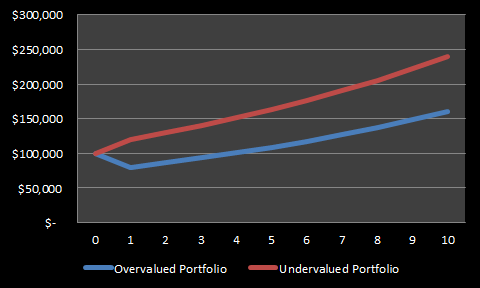

Consider two investors that each invested $100,000 in dividend portfolios with 5% starting yields. Over the course of ten years each investor realizes annual dividend growth of 3%. The first investor (blue line) bought stocks that were considerably overvalued and subsequently lost 20% in capital value in year one; alternatively, the other (red line) invested in stocks that were undervalued and gained 20% in capital value in year one.

After the year one corrections to fair value, both portfolios grow at 8% per year through year 10.

At the end of ten years, both portfolios generated the same amount of dividend income ($57,319), but their ending capital values are nearly $80,000 apart ($159,920 vs. $239,880). It's hard to imagine that the two investors would feel equally good about their performance even though they realized equal dividend income over the ten year period.

To further my point, if both investors decided to liquidate their dividend portfolios in year 10 and invested their capital in bonds with 5% coupons, the first investor would receive annual payments of $7,996 while the second investor would receive $11,994 per year until maturity.

This is an admittedly simple example, but it illustrates an important point about the hidden costs of not paying attention to valuation in income investing. Ultimately, capital growth matters.

Valuation avoidance (Photobucket)

Whether you use relative valuation methods (i.e. comparing P/E ratios, etc.) or absolute valuation methods (i.e. dividend discount models, discounted cash flow models, etc.), the important thing is to fully consider the price you're paying and the value you're getting from each investment. Get to know the businesses you'd like to invest in, understand what drives their performance, and don't rely on a single metric -- in this case, dividend yield -- to guide your buying decisions.

A mildly non-conventional investment approach, emphasizing a business approach to security selection, gives some opportunity for long-term results slightly above average without corresponding increase in investment risk. - Warren Buffett

If you think this article may be of interest to a friend or colleague, feel free to forward it, and let me know if you have any questions about topics discussed. Best, Todd

@toddwenning

There was big news today in the income investing world as UK fund manager Neil Woodford announced he will leave Invesco Perpetual in 2014, after managing money there for 25 years. When I first saw the headline, I thought he might be pulling a Peter Lynch and retiring at the top, but no, he's just setting up his own firm. Though Woodford is less well known in the US, his track record at Invesco Perpetual is top-shelf by any standard and he's the industry's best-known (and perhaps best overall) income investor. As such, I'm looking forward to hearing more from him and learning more about his investing approach once he's established the new firm.

For now, I've put together a list of some of my favorite Neil Woodford quotes:

I look to invest in businesses that can provide sustainable long-term dividend growth. If I can invest in a businesses when its growth potential is not reflected in the valuation of its shares, this not only reduces the risk of losing money, it increases the upside opportunity.

In the short-term, share prices are buffeted by all sorts of influences, but over longer-time periods fundamentals shine through. Dividend growth is the key determinant of long-term share price movements, the rest is sentiment.

The economic outlook is tough and will stay so for some time. But the current yield available on selected stocks, combined with dividend growth, can provide decent returns. If you can invest at very low valuations, returns could be even more meaningful. Equity markets offer an attractive yield for investors looking for a better return on capital. This return is not risk free, but a selective and patient approach helps to mitigate risks.

I am...absolutely convinced that, in the long-term, valuation and fundamentals of a company are the only things that matter and, like gravity, those things will reassert themselves.

We do not focus on short-term performance issues; we focus on the valuation of fundamentals. Our disciplined approach guides us, we believe, to the best opportunities in the stock market and we are very patient investors. We expect our performance to improve when the market begins again to focus, as it inevitably will, on valuation.

I am not sure that I have ever really identified a catalyst that has changed anything...the catalyst that I focus on most of all is valuation; valuation is the only catalyst that I really trust.

The biggest challenge for me, I suppose, is holding my nerve...But I’m afraid you are condemned by your process and what you believe in, and you have to stick to those as a fund manager or you’ve got nothing to hold on to. We believe in what we are doing. I believe what I’m doing,

When we communicate with our investors, what we’re saying is don’t measure us on the basis of 6 months or a year. Look at us over a 3 to 5 year period. And if we can’t deliver those absolute positive returns, then vote with your feet.

The great architect Frank Lloyd Wright aimed for "the elimination of the insignificant" in his designs rather than try to dazzle the viewer with ornaments, extra rooms, and unnecessary complexity.

Clearly this didn't mean that his work was dull or uninspired.

Fallingwater by FLW. (Photo by K Wenning)

The ultimate aim of the investor should also be to simplify.

I'm not saying investing is simple -- far from it. But as we build experience, improve our skills, and perhaps have a little success, the temptation to make investing more complex increases, and the industry is more than happy to provide you with options to make it more complex than it needs to be.

As Vanguard founder Jack Bogle writes in Enough: "Financial institutions operate by a kind of reverse Occam's razor. They have a large incentive to favor the complex and costly over the simple and cheap, quite the opposite of what most investors need and ought to want."

From the industry's perspective, our strategy of focusing on income, buying good businesses at good prices, and monitoring our positions with the aim of holding for five-plus years might seem quaint, and perhaps even a little naive. We know different, of course, but then again we're not their target customers.

In our quest to become better investors, we should remember Wright's approach of eliminating the insignificant from our work. New research tools and investment vehicles can be great, but they must assist us in simplifying our processes rather than make them more complicated.

In 2005, I distinctly recall perusing the Barnes & Noble business section for a book on dividend investing, only to find just one book that specifically addressed the topic. (There are, um, quite a few more available today on Amazon.com.)

Things changed with the financial crisis, as we know. Interest rates plunged and dividend stocks rapidly became an attractive alternative for income-seeking investors. Indeed, the Google Trends chart for the search term “dividend stocks” illustrates the changes in sentiment from 2004 to present quite nicely:

Source: Google Trends

Naturally, the financial services industry responded to strong investor demand for dividends by launching dividend-themed ETFs, ETNs, and funds to attract assets. Some are more creative than others, but when there's a revenue-weighted dividend ETF (not kidding), you know folks are running out of ideas.

Fortunately, it seems we're past the "peak" for dividend valuations, investor interest appears to be turning elsewhere, and more long-term buying opportunities could thus present themselves.

"Non-dividend stocks have outperformed dividend stocks in the S&P 500 over a one year timeframe. Prior to this period, nonpayers had underperformed dividend stocks since late 2009." - FactSet Dividend Quarterly, September 2013

Just this week, in fact, I started a position in Coca-Cola -- my first buy this year for the dividend sleeve of my portfolio -- and found it interesting that the stock was yielding over 3% for the first time since 2010. Though low interest rates may be around a little longer, the prospect of rising interest rates in the coming years should at least limit further multiple expansion for higher-yielding dividend stocks. In the event of a market pull-back and considering the robust dividend growth we've seen in the last three years, I would expect to see more quality 3% to 5% yields coming available. Stay focused and patient out there. Best, Todd @toddwenning Good reads this week

"My father was very sure about certain matters pertaining to the universe. To him, all good things -- trout as well as eternal salvation -- come by grace and grace comes by art and art does not come easy." -- Norman Maclean, "A River Runs Through It"

I sometimes think we are too much impressed by the clamor of daily events. Newspaper headlines and the television screens give us a short view...Yet it is the profound tendencies of history, and not the passing excitements, that will shape our future. —JFK

A few years ago, I was speaking with one of my favorite fund managers and asked him why he chose to set up shop in a small town, hundreds of miles from Wall Street. His answer was simple: "In order to focus."

The perfect place to invest?

The more immersed you are in investing, the more distractions there are. It's just that simple. Great investors find a way to focus and tune out the distractions. For some, like the fund manager, that might mean living away from the hustle and bustle of major cities. Before you put up the "for sale" sign... Knowing how to separate what's important and what isn't partially comes with experience and going through a few market cycles, but investors at any level can dramatically improve their decision-making process by simply not investing with the news cycle. A few weeks ago, Josh Brown (aka Reformed Broker) had a great post entitled "I Went to Cash Because (Please Check One)". It does a great job of showing that investors who sold their stocks based on passing story lines over the last few years have ended up being sorry. The news cycle can be intense at times -- in both up and down markets -- and it's easy to get caught up in it. The key thing to remember is to not make investing decisions based on the news topic du jour. Like the Chicago weather, just wait a few minutes and it'll change. What really matters Alternatively, as JFK's quote suggests, it's the "profound tendencies of history" that really matter in the long-run. JFK was commenting about society and politics, of course, but I believe the principles also apply to investing and business. Over time, individual companies, sectors, and markets will be shaped by things like competitive dynamics, investment, and innovation. It certainly isn't whether or not Republicans are disagreeing with Democrats at the moment. As such, you can dramatically improve your investment focus by paying more attention to factors that affect longer-term profitability. One thing's for sure -- these factors won't be found in the news cycle. Best, Todd @toddwenning

1. Income investing is a separate and distinct strategy

It's not growth, it's not value -- income comes first. (See: The Income Investor's Manifesto)

2. Discipline and patience are behavioral prerequisites

Great dividend-producing portfolios are built over decades, not weeks and months. It's critical to keep short-term market moves in perspective. (See: Making Each Investment Count)

3. Insist on owning dividend-paying companies with economic moats

You'll save yourself a lot of trouble if you own firms with durable competitive advantages. Read this book to learn how to recognize an economic moat. 4. Keep transaction costs to a minimum

Ideally below 1% per year. Remember: you can only compound what you keep.

5. Beware of unrealistic yields

If a yield seems too good to be true, it probably is. There might be something wrong with a stock that carries a yield more than twice the index average. (See: Ultra High Yield = Ultra High Risk)

6. Don't be afraid to sell, but do so for the right reasons

Trading and income investing don't mix. Take an investor's perspective and aim to hold for at least three years. (See: A Simple Guide for Selling Stocks)

7. Have a dividend reinvestment strategy

How you manage the regular cash flows from your dividend portfolio can have a tremendous impact on your long-term returns. (See: 5 Keys for Reinvesting Dividends) 8. Think globally, but be mindful of extra costs

There are great dividend opportunities in foreign markets, but be aware of possible withholding taxes in the company's home country. 9. Stay away from companies drowning in debt

Companies with too much debt become beholden to creditors and the dividend can come under pressure if the creditors aren't satisfied.

10. Take a portfolio perspective

A dividend strategy isn't comprised of one or two stocks, but rather a group of stocks assembled to achieve specific objectives and goals. (See: 5 Rules for Building a Dividend-Focused Portfolio)

What do you think? Any points to add? Please let me know in the comments section below.

Over the last two weeks, we've been searching for promising dividend growth stocks that trade on the U.S. markets. Our original objective was to identify "quality dividend-paying small- to mid-cap companies with sustainable competitive advantages and the potential for 7%+ annual dividend growth over the next 7-10 years." After running a broad screen to reduce the number of initial contenders, we put six companies through the Dividend Compass spreadsheet to get a better feel for the health of the companies' dividends. Of course, all of that work was based on historical data. Today, we'll dig deeper into the two finalists -- MTS Systems and WD-40 Company -- to determine how those names might perform going forward. Further, the research we've already done shows that both companies have solid balance sheets, are consistent generators of free cash flow, and have established good dividend track records. As such, we won't spend too much time digging into those data points today. Instead, we'll look at the two companies' competitive advantages (if they indeed exist), management quality, and consider their current valuations to determine whether or not they're worthy of investment right now. The finish line is in sight After digging into WD-40 and MTS this week, it's clear that the screening and Dividend Compass process uncovered two promising companies. Indeed, they check off a number of Peter Lynch's 13 signs of a perfect stock. Among them: little analyst coverage (officially, MTSC has two analysts, WDFC has four analysts), they each have a niche, and the companies are buying back stock (though this isn't always a great thing, in my opinion). As with most endeavors, the hardest part of the investing process is the last stretch. Most investors go through the screening process and read historical financial statements. Where you can separate yourself as an investor is in this last stretch of research -- digging for the qualitative factors and getting a feel for valuation.

MTS Systems (MTSC)

What does the company do?

MTS Systems supplies test systems and industrial sensors to a number of end-markets such as the automotive, aerospace, fluid power, and manufacturing sectors (i.e. mostly cyclical industries). About 80% of revenue comes from the test segment, which designs force and motion systems for determining a new product's mechanical properties; MTS commands a 16% market share of the global testing product and service industry. The sensors segment helps customers improve the efficiency and safety of their automated manufacturing processes and also measures fluid displacement and liquid levels; MTS has a 6% share of the global sensors market.

Source: MTS

MTS also has a wide geographical reach, with an established presence in the world's major manufacturing centers.

Source: MTS

Does it have sustainable competitive advantages?

Historical financials seem to suggest that MTS has a sustainable competitive advantage. It may lie in the "mission critical" nature of its products. Firms investing many millions of dollars in large industrial products simply cannot afford to forgo strenuous mechanical and fatigue testing before rolling the new product out to customers. The warranty or recall risk from a flawed piece of equipment may well outweigh the testing cost. Further, some products may be required to undergo such testing due to government regulation. But these could simply be industry-level advantages rather than a specific advantage to the firm.

Where MTS may set itself apart is with its established brand and reputation in the industry for doing quality testing, particularly for larger-scale projects. I'd imagine that most smaller-scale product testing can be done internally and that the competition for smaller-scale projects is pretty fierce. Larger-scale testing projects can last up to three years, however, and there are probably only a few companies that can handle such work -- MTS being one of them -- and customers are unlikely to switch providers halfway through the testing period. As such, I'd say MTS has a slight advantage stemming from switching costs for larger projects, but the depth of the moat will fluctuate along with demand for these larger-scale projects.

How about management?

The MTS leadership team is relatively new, by which I mean less than two years in their roles. It seems a few years ago that the company got in a little trouble regarding some disclosure items relating to government contracts. This appears to have been one of the primary drivers behind the August 2011 resignation of the former CEO and the re-shuffling of the executive suite. Such dramatic moves are necessary when there's been an ethics issue, but it also likely means that the company will be in transition mode for a few years. Unless you know a lot about the new management team (I don't) and the effect the changes are having at the ground level (again, I don't), it's hard to make a bold turnaround call (so I won't).

Short-term cash bonus metrics are based on EPS, EBIT, revenue, and orders. Not my favorite set of metrics, but not terrible given that MTS remains squarely in the growth stage of its lifecycle. In time, I'd prefer to see less emphasis on top-line growth and more emphasis on free cash flow and profit growth.

Biggest concern?

With 40% of testing orders coming from Asia, I have some concerns regarding the Chinese economy -- specifically, how the shift from an investment- and manufacturing-driven economy to a customer-driven one may affect demand for MTS's testing services in the region. MTS aims to double its revenue to $1 billion by 2018 and robust demand from the Chinese market will likely be necessary to achieve that goal.

Is it a good buy today?

MTS's average return on equity over the last five years is about 18% and its dividend policy is to pay out approximately 30% of earnings, implying a back-of-the-envelope sustainable growth rate of between 12-13%. Not bad against a P/E ratio of 18.6 times (~1.5 PEG), but not a slam dunk, either.

Doing some DCF work on MTS with a range of reasonable growth assumptions, I'd put a base case fair value near $60 per share, which is in-line with today's market price. I'd need a margin-of-safety of at least 20% with this type of business, so a good entry point might be closer to $48.

MTS is definitely a good one to watch in the event of a market pullback and there's significant dividend growth potential, but given my uncertainty around its sustainable competitive advantages and a newer management team, I wouldn't make it more than 2% of my portfolio.

WD-40 Company (WDFC)

What does the company do?

Anyone who's spent time in a garage, fixing squeaky hinges around the house, or worked on bicycles has likely used a WD-40 product. In fact, the vast majority of the company's revenues are based on the original WD-40 formula (WD-40 stands for “Water Displacement perfected on the 40th try”) and the company's documented over 2,000 uses for the secret formula. The company also owns a number of related consumer/industrial cleaning products such as Lava soap and X-14 mildew stain remover. Its products are sold in 187 countries, so the company does have a wide geographic reach (about 40% of sales are U.S.-based).

Does it have sustainable competitive advantages?

For starters, the WD-40 brand name is extremely valuable. I can't even name a substitute product. It's a trusted brand, can charge a premium price, and I'd even argue that there's a slight emotional connection to the brand (i.e. "this is the brand that my dad always used in the garage"). Beyond the brand, the company's ability to build upon a single secret formula and create multiple products is an example of economies of scope. This results in a cost advantage that would-be competitors would struggle to match if they attempted to go head-to-head with WD-40 on a certain product line.

Source: WD-40

The company's ability to consistently generate double-digit returns on capital is another indication that an economic moat is likely present. Finally, another telling statistic: in 2012, WD-40 generated nearly $1 million in revenue per employee. I like to see at least $250,000 in revenue per employee, so this is definitely a sign of a strong company.

How about management?

One thing that I really like about WD-40's management team is that all seven corporate officers been with the company for more than 15 years. My personal preference is for the companies I own to promote from within and to have a deep bench of talent in the event an executive leaves or retires. This is particularly true for a company with a strong corporate culture, as it supports cultural continuity. Now, a company with a rotten corporate culture may need to hire an outsider to shake things up, but all else equal I prefer internal promotion in the executive suite.

CEO Garry Ridge has been with the firm since 1987 and the CEO since 1997. During his tenure, the stock is up 319% cumulative, or about 9.2% annualized, compared to a 200% gain, or 6.9% annualized, for the S&P 500 over the period. The stock's also outperformed the S&P 500 by about 40 percentage points over the last five years. All this is to say that long-term shareholders should be fairly happy with the way the company's performed under Ridge's leadership. WD-40 also keeps the chairman position separate from the CEO role, which is textbook best practice for corporate governance.

I'm not crazy about management's bonus incentives, which are primarily linked to EBITDA. EBITDA is one of my least favorite financial metrics (Buffett called trumpeting EBITDA a "pernicious practice" in the 2002 letter; Munger called it "(expletive) earnings") because interest, taxes, and depreciation are natural and recurring shareholder expenses that shouldn't be ignored. I could rant on about EBITDA, but I'd much prefer this otherwise high quality company to use more shareholder-focused incentive metrics such as net income, free cash flow, and/or economic value added (EVA).

Biggest concern?

A potentially limited growth runway. With its products already in 187 countries and a sizeable portfolio of products already built around the WD-40 brand, what will drive top-line growth in the medium-term? I have no doubt that consumers will continue to buy WD-40, but can the company deliver high-single digit/low-double digit earnings growth without becoming more active on the M&A front?

Is it a good buy today?

WD-40's consistency and high quality hasn't been overlooked by the market and the stock has historically traded at a premium. WD-40's five-year average P/E is 19.1 times versus 17.2 times for the S&P; today it's trading at 22.7 times. Not exactly cheap on that basis. But what about growth? Based on the company's five-year average return on equity near 19% and its dividend payout ratio near 50%, the "sustainable growth rate" is about 9-10%. An implied PEG ratio near 2x isn't great, either. Its current dividend yield of 2.1% is also well-below its five year average closer to 3%.

Running a quick valuation on WD-40, I put a fair value on the shares at $52 (currently $58.52). I'd look to buy with at least a 15% margin-of-safety, so a good buy-around price today would be $44.

I really like WD-40 as a company. Hopefully the EBITDA-based incentive metrics go away, but otherwise I'd be happy to own WD-40 in the event of a market pullback. Ideally, I'd like to pick up the stock with a yield closer to 3%, which is about what I'd get if the stock traded near $44.

Bottom line

MTS Systems and WD-40 are both intriguing dividend growth candidates, but neither appears to be a good value at the moment. MTS has more dividend growth potential than WD-40, but also carries more risk.

All in all, I think this was a worthwhile exercise. We dug into two promising dividend growth opportunities and now have two good names to keep on our watchlists.

What do you think? Please let me know in the comments section below. Note: I switched the comments format back to the normal setting as the Google+ format was simply not working well. You can also reach me @toddwenning on Twitter.

.png)